TL;DR / Quick Summary

A personal injury lawsuit loan is a type of pre-settlement funding that allows access to a portion of an expected settlement before the case is resolved. It is non-recourse, which means repayment is required only if the case is successful.

In this guide, you’ll learn:

- What personal injury lawsuit loans are in simple terms.

- How the funding process works from start to finish.

- When this option is used during a case.

- What to consider before applying.

A personal injury lawsuit loan exists to solve a timing problem. A claim may already have value, but access to that money depends on when the case settles, not when expenses arise.

The U.S. Bureau of Justice Statistics reports that civil cases, including personal injury claims, can take months or even years to resolve depending on complexity and negotiation. During this period, financial obligations continue without delay.

This delay means the value of a claim exists, but access to that money does not. Personal injury lawsuit loans are designed for this stage, allowing a portion of the expected settlement to be accessed before the case is resolved.

In this guide, we will explain what a personal injury settlement loan is, how it works, and how to evaluate whether it fits a given situation.

What Is a Personal Injury Settlement Loan?

A personal injury settlement loan is a way to access part of a settlement before a case is resolved. It is based on the expected value of the claim and is typically used when there is a delay between ongoing expenses and the final payout.

These are commonly known as personal injury lawsuit loans, pre settlement loans, or settlement cash advances. While the terminology varies, the structure remains the same. The funding is tied to the case, not personal credit or income.

One key detail often misunderstood is that this is not a traditional loan. It is a non-recourse advance. Repayment is required only if the case results in a settlement or verdict. If there is no recovery, there is no repayment obligation.

This is why personal injury loans on settlements are approached differently from bank loans or credit-based options. The decision is based on the strength of the legal claim and its likely outcome.

Looking at how pre-settlement funding compares with other options could be beneficial for ones evaluating and making decisions.

How Personal Injury Settlement Loans Fit Into the Legal Process

A typical personal injury case moves through investigation, treatment, negotiation, and eventual settlement. This entire process can take time depending on the personal injury cases timeline.

Now let’s understand how it works in practice, the process follows a clear sequence:

Application and case review

The process begins with sharing basic details about the case along with attorney information. This allows the provider to understand the stage of the claim and begin an initial review. In most cases, the attorney is involved early to confirm case status and documentation, which helps move things forward without delays.

Evaluation based on case strength

The focus here is on the case itself. Providers look at liability, expected settlement value, and how far the case has progressed. This is what determines eligibility. Credit score, employment, or personal financial history are not part of the evaluation.

Offer based on expected settlement

If the case meets the criteria, an offer is made based on its projected value. Most loans against personal injury claims are structured as a percentage of the expected settlement rather than a fixed loan amount.

Funding and access to cash

Once the offer is accepted, funds are released. The process is usually quick when documentation is complete and the case details are clear.

Repayment after settlement

Repayment happens only after the case is resolved. The amount is deducted directly from the settlement, so there are no monthly payments during the case. If there is no recovery, there is no repayment obligation.

At this stage, it also helps to understand when this option becomes necessary. In many cases, it aligns with situations where pre-settlement funding becomes necessary, especially when financial pressure starts affecting decision-making.

What Types of Cases Qualify for Personal Injury Settlement Loans?

Not every legal claim qualifies for personal injury lawsuit loans. Approval depends on the strength of the case, clear liability, and the likelihood of a settlement.

Most funding providers look for cases where there is a defined injury, ongoing treatment, and a reasonable expectation of compensation. The stronger and more documented the case, the higher the chances of approval.

Common case types that qualify include:

- Car accidents and motor vehicle collisions.

- Slip and fall or premises liability cases.

- Medical malpractice claims.

- Product liability and defective product injuries.

- Workplace injuries and workers’ compensation claims.

- Wrongful death cases.

In addition to the type of case, timing also matters. Cases that are already filed or moving through negotiation tend to be evaluated more quickly, since there is more clarity around potential outcomes.

Understanding the value of a claim can also make a difference when considering funding. For example, reviewing strategies like ways to get a better settlement can help strengthen the position of a case before exploring funding options.

The Pros and Cons of Personal Injury Lawsuit Loans

Before moving forward with personal injury settlement loans, it helps to look at both sides clearly. These funding options can be useful in the right situation, but the trade-offs matter just as much.

The table below gives a clear view of what to expect:

| Basis | Benefits | Considerations |

| Access to funds | Funds are available while the case is ongoing. | Amount is limited to a portion of the expected settlement. |

| Repayment structure | No repayment if the case is unsuccessful. | Repayment comes from the final settlement amount. |

| Eligibility | No credit checks or income requirements. | Approval depends on case strength and documentation |

| Financial impact | Helps manage expenses without early settlement pressure. | Fees and costs can increase overtime. |

| Control over decision | Allows more time to negotiate a fair outcome. | Taking more than needed can reduce net recovery. |

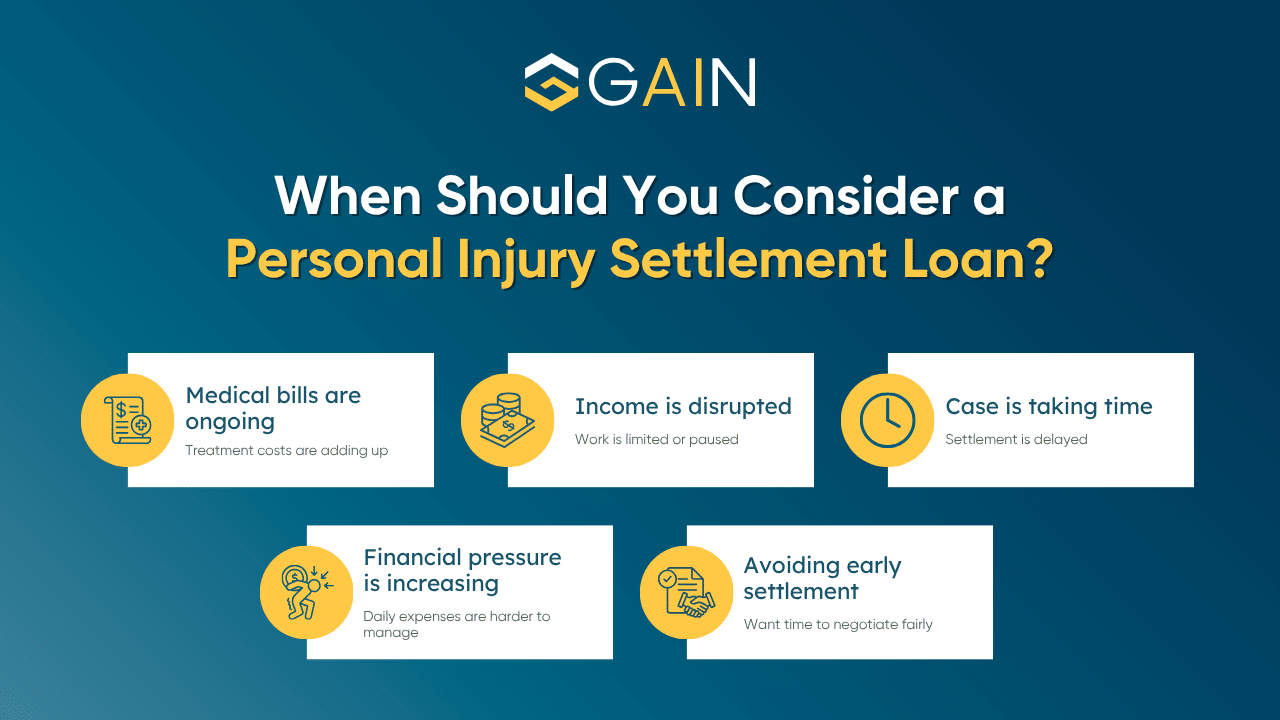

Is a Personal Injury Settlement Loan Right for You?

This usually comes down to timing and financial pressure. When expenses are building and the case is still ongoing, waiting may not always be practical. In those situations, accessing part of the settlement early can help maintain stability without affecting the direction of the case.

At the same time, this is not something to rush into. The value of the claim, the stage of the case, and the amount needed all matter. Taking a smaller amount, rather than the maximum available, often works better in the long run.

It is also important to align this decision with the legal side of the case. A quick discussion with the attorney handling the claim can bring clarity on expected timelines and settlement value. This makes it easier to decide whether funding fits the situation or not.

For a clearer sense of when this option becomes relevant, it helps to look at situations where pre-settlement funding becomes necessary, especially when financial pressure starts influencing decisions.

How to Apply for a Personal Injury Settlement Loan

The process of applying for personal injury lawsuit loans is usually simple and structured. Most providers are set up to move quickly, especially when the case details are already in place.

Here’s what the process mainly involves:

- Basic case details:

Information about the case, including the type of injury, attorney details, and current stage, is shared. This gives the provider a starting point to understand the claim. - Attorney coordination:

The provider connects with the attorney to verify case status and gather supporting documents. This step helps move the process forward without delays. - Case review and approval:

The evaluation focuses on liability, expected settlement value, and how far the case has progressed. Approval depends on the strength of the claim, not credit history. - Offer and terms:

Once approved, an offer is made based on the case value. Terms, fees, and repayment structure are outlined clearly before moving ahead. - Funding timeline:

After acceptance, funds are released. In most cases, this happens quickly when documentation is complete. - Repayment structure:

Repayment is made directly from the settlement once the case is resolved. If there is no recovery, there is no repayment obligation.

To see how this works in practice, it helps to review how pre-settlement funding is structured for plaintiffs. For cases that need faster approvals, guaranteed pre-settlement funding options can also be explored depending on eligibility.

Conclusion

A personal injury lawsuit loan is not something every case needs, but in the right situation, it can make a meaningful difference. It allows access to funds during a period where the case has value, but the payout is still pending.

What matters most is clarity. Understanding how the funding works, how much is actually needed, and how it affects the final settlement helps in making a balanced decision. When used carefully, it can reduce financial pressure without changing the direction of the case.

For those considering this option, the next step is to explore how it applies to a specific case. Learn more about available options or get started directly at Gain Servicing.

FAQs

Best personal injury lawsuit loan companies

The best providers are those that offer clear terms, transparent pricing, and work closely with attorneys. A reliable company focuses on case strength rather than credit and keeps the process simple and easy to understand.

How do lawsuit loans work for personal injury cases?

They are advances based on the expected settlement. The provider reviews the case, makes an offer, and releases funds. Repayment happens only if the case is successful and is deducted from the final settlement.

Where can I apply for a personal injury settlement advance online?

Applications are typically completed online through funding providers. Most require basic case details and attorney information to begin the evaluation and approval process.

Eligibility requirements for personal injury funding

Eligibility depends on the strength of the case, clear liability, and expected settlement value. Credit score, income, and employment status are generally not part of the approval criteria.

What are the typical interest rates for legal funding?

Rates vary based on the provider and case risk. Costs can increase over time, so it is important to review the terms carefully and understand the total repayment before accepting an offer.